USA Medicare Part A vs Part B Explained (Complete Beginner’s Guide – 2026)

If you’re approaching retirement or helping a family member sign up for healthcare, you’ve probably heard about Medicare Part A and Medicare Part B. But many Americans still ask the same question:

“What’s the difference between Medicare Part A and Part B?”

Understanding the difference is super important because these two parts form the foundation of Medicare health coverage in the United States.

Both plans cover different types of healthcare services. Together, they help millions of Americans pay for hospital visits, doctor appointments, and essential medical care.

In this guide, we’ll break down Medicare Part A vs Part B in simple terms, explain what each plan covers, how much they cost, and how you can decide which option is right for you.

Let’s dive in.

What Is Medicare?

Before comparing Part A and Part B, let’s quickly explain what Medicare actually is.

Medicare is a federal health insurance program in the United States designed mainly for:

- Adults age 65 and older

- Individuals with certain disabilities

- People with serious health conditions like kidney failure

The program was introduced in 1965 and now provides healthcare coverage for more than 65 million Americans.

Medicare is divided into four main parts:

- Part A – Hospital Insurance

- Part B – Medical Insurance

- Part C – Medicare Advantage

- Part D – Prescription Drug Coverage

In this article, we’re focusing on the key differences between Medicare Part A and Part B coverage.

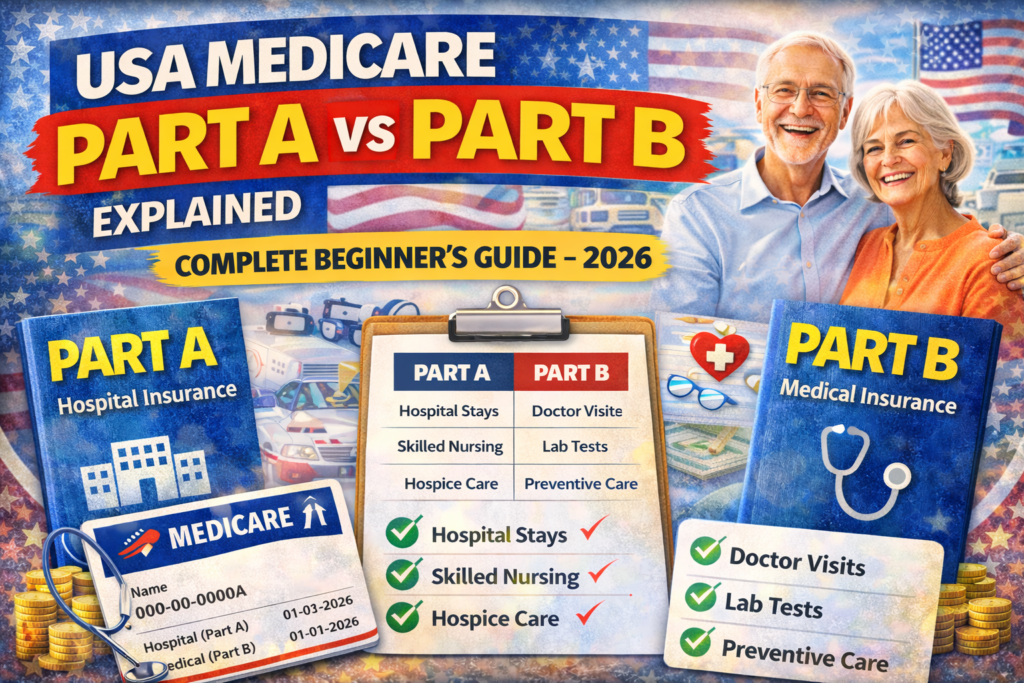

What Is Medicare Part A?

Medicare Part A is often called hospital insurance.

It helps pay for healthcare services when you are admitted to a hospital or medical facility.

Medicare Part A covers:

- Inpatient hospital stays

- Skilled nursing facility care

- Hospice care

- Limited home health services

This coverage is designed to help pay for major medical events that require hospitalization.

Examples of Medicare Part A Coverage

Here are some real-life examples of when Medicare Part A might apply:

- You stay overnight in a hospital after surgery

- You receive hospice care for a terminal illness

- You need rehabilitation in a skilled nursing facility

- You require short-term home healthcare after hospital discharge

These services can cost thousands of dollars without insurance.

That’s why Medicare hospital coverage plays a crucial role in protecting seniors from massive medical bills.

How Much Does Medicare Part A Cost?

The good news is that many Americans qualify for premium-free Medicare Part A.

You typically don’t pay a monthly premium if:

- You worked and paid Medicare taxes for at least 10 years

- Your spouse paid Medicare taxes for 10 years

However, there are still out-of-pocket costs, including:

- Deductibles

- Coinsurance

- Copayments

Hospital deductibles can change each year, so it’s important to check the latest rates.

What Is Medicare Part B?

Medicare Part B is known as medical insurance.

While Part A focuses on hospital care, Part B covers outpatient medical services.

This includes healthcare you receive outside of a hospital stay.

Medicare Part B Covers:

- Doctor visits

- Preventive care

- Lab tests

- X-rays and imaging

- Ambulance services

- Mental health services

- Medical equipment

- Physical therapy

Part B is designed to help cover routine medical care and doctor services.

Examples of Medicare Part B Coverage

Here are common situations where Medicare Part B applies:

- Visiting your primary care doctor

- Getting blood work or lab tests

- Receiving flu shots or vaccines

- Getting a cancer screening

- Using medical equipment like wheelchairs

- Receiving outpatient surgery

These services are extremely common, which is why most Medicare beneficiaries enroll in Part B.

How Much Does Medicare Part B Cost?

Unlike Part A, Medicare Part B requires a monthly premium.

The premium amount may vary based on income.

For many Americans, the monthly premium is around:

$170 to $200 per month

You may also pay:

- Annual deductibles

- 20% coinsurance for most services

Even though there are costs, Part B is essential because it covers regular healthcare services seniors rely on.

Key Differences Between Medicare Part A and Part B

Now let’s compare Medicare Part A vs Part B coverage side by side.

| Feature | Medicare Part A | Medicare Part B |

|---|---|---|

| Coverage Type | Hospital insurance | Medical insurance |

| Covers | Hospital stays | Doctor visits |

| Premium | Usually free | Monthly premium |

| Services | Inpatient care | Outpatient care |

| Examples | Surgery, hospice | Checkups, lab tests |

Together, these two parts create what’s known as Original Medicare.

Do You Need Both Medicare Part A and Part B?

In most cases, the answer is yes.

Both plans cover different types of medical services.

Without Part B, you would have to pay out-of-pocket for:

- Doctor visits

- Diagnostic tests

- Preventive screenings

Without Part A, hospital stays could become extremely expensive.

Most Americans enroll in both Medicare Part A and Part B when they turn 65.

When Should You Enroll in Medicare Part A and Part B?

Your Initial Enrollment Period begins around your 65th birthday.

This enrollment window lasts seven months:

- Three months before your birthday

- Your birthday month

- Three months after your birthday

Signing up during this time helps avoid late enrollment penalties.

What Happens If You Delay Medicare Part B?

If you delay Part B without having other qualified coverage, you may face lifetime penalties.

The penalty usually increases your premium by 10% for each year you delayed enrollment.

That’s why experts recommend enrolling on time unless you have employer coverage.

What Medicare Part A and Part B Do NOT Cover

Although Medicare covers many services, it does not cover everything.

Some services that Original Medicare typically does not include are:

- Routine dental care

- Vision exams for glasses

- Hearing aids

- Long-term nursing home care

- Cosmetic procedures

Because of these gaps, many Americans buy Medicare Supplement Insurance (Medigap).

Medicare Supplement Insurance (Medigap)

Medigap policies help cover costs that Original Medicare does not fully pay.

These may include:

- Deductibles

- Coinsurance

- Copayments

Medigap plans are offered by private insurance companies.

They are popular among seniors who want extra protection from unexpected healthcare costs.

Medicare Advantage Plans

Some people choose an alternative called Medicare Advantage (Part C).

These plans bundle:

- Part A

- Part B

- Often Part D

They may also include extra benefits like:

- Dental coverage

- Vision coverage

- Fitness programs

However, Medicare Advantage plans typically require using a specific network of providers.

Tips for Choosing the Right Medicare Coverage

If you’re deciding between Medicare options, here are some helpful tips.

Evaluate Your Health Needs

Consider your current medical conditions and prescriptions.

Compare Medicare Plans Carefully

Different plans offer different benefits and costs.

Check Provider Networks

Some plans require using specific doctors and hospitals.

Understand Out-of-Pocket Costs

Compare premiums, deductibles, and coinsurance.

Frequently Asked Questions

Is Medicare Part A really free?

Yes, most Americans qualify for premium-free Part A if they paid Medicare taxes for at least 10 years.

Do I have to enroll in Medicare Part B?

No, but most people do because it covers essential healthcare services like doctor visits and outpatient care.

Can I have Medicare Part A without Part B?

Yes, but it’s not common. Without Part B, you would pay out-of-pocket for most routine medical care.

What is the biggest difference between Medicare Part A and Part B?

Part A covers hospital care, while Part B covers doctor visits and outpatient services.

Can I add prescription drug coverage later?

Yes. Medicare Part D plans can be added for prescription drug coverage.

Final Thoughts

Understanding Medicare Part A vs Part B in the United States is one of the most important steps in preparing for retirement healthcare.

Part A focuses on hospital coverage, helping pay for inpatient care and medical facilities. Part B covers doctor visits, preventive services, and outpatient treatment.

Together, they create the foundation of Original Medicare, which provides essential healthcare coverage for millions of Americans.

By learning how these two plans work, you can make smarter healthcare decisions and ensure you have the right protection when you need it most.