In-Network vs Out-of-Network Doctors Explained (Complete Guide for Americans – 2026)

Choosing the right doctor in the United States isn’t just about who has the best reviews or the closest office. When it comes to health insurance, one of the most important things to understand is the difference between in-network and out-of-network doctors.

If you’ve ever looked at your medical bill and thought, “Why is this so expensive?”, chances are it had something to do with whether your doctor was in your insurance network.

In this guide, we’ll break down in-network vs out-of-network doctors explained in simple terms, with real-life examples, tips to save money, and answers to common questions Americans ask about health insurance networks.

Let’s dive in.

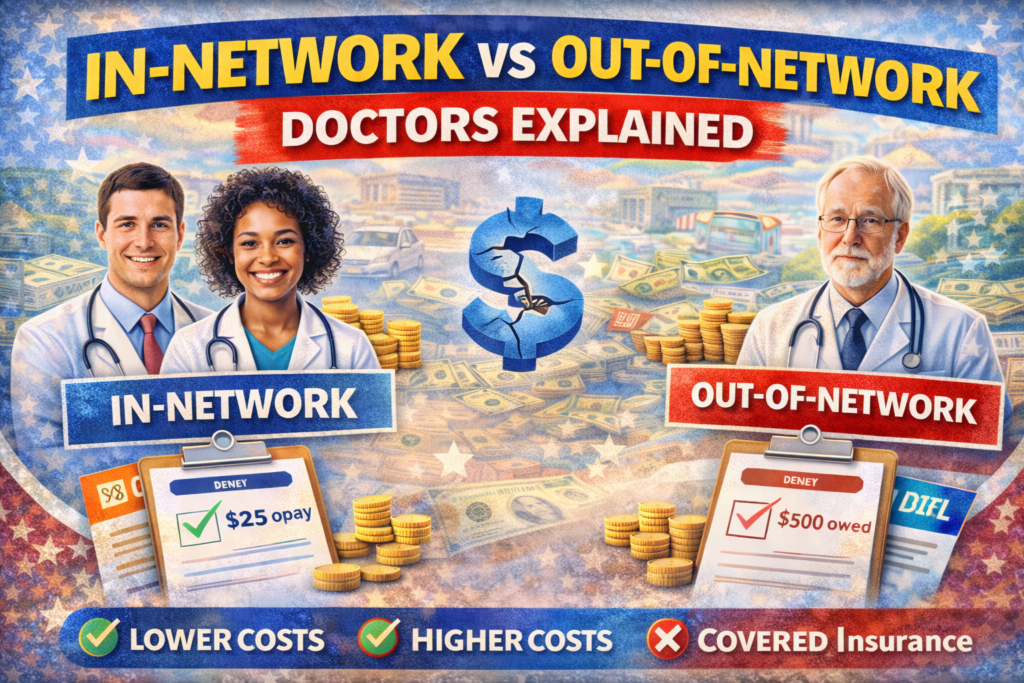

What Does “In-Network” Mean in Health Insurance?

An in-network doctor is a healthcare provider that has a contract with your health insurance company to provide services at negotiated rates.

In simple terms:

- Your insurance company pre-approves the doctor

- The doctor agrees to lower prices for insured patients

- You usually pay less out of pocket

Insurance companies negotiate these prices to keep healthcare costs under control.

Example

Let’s say a doctor charges $200 for a visit.

If the doctor is in-network:

- Insurance negotiates the price to $120

- Your copay might be $25

- Insurance pays the rest

So instead of paying $200, you only pay $25.

Pretty sweet deal, right?

What Does “Out-of-Network” Mean?

An out-of-network doctor is a healthcare provider that does NOT have a contract with your insurance company.

That means:

- The doctor sets their own price

- Your insurance may cover less

- You might pay much more

Sometimes your insurance may not cover out-of-network care at all, depending on your plan.

In-Network vs Out-of-Network Doctors: Key Differences

Here’s a simple comparison that explains everything clearly.

In-Network Doctors

- Contracted with your insurance company

- Lower negotiated prices

- Smaller copays

- Claims filed automatically

- Less paperwork for patients

Out-of-Network Doctors

- No contract with your insurance

- Higher medical costs

- Larger out-of-pocket payments

- You may need to file claims yourself

- Insurance coverage may be limited

This is why understanding in-network vs out-of-network healthcare providers in the USA is crucial for avoiding surprise medical bills.

Why Insurance Networks Exist

Health insurance companies create provider networks to control costs and manage healthcare services.

These networks include:

- Doctors

- Hospitals

- Specialists

- Labs

- Pharmacies

By negotiating rates with providers, insurance companies can:

- Reduce healthcare costs

- Offer lower premiums

- Provide predictable pricing

For patients, this means cheaper medical care when staying inside the network.

Types of Health Insurance Plans and Network Rules

Different health insurance plans have different network rules.

Here are the most common types in the United States.

HMO (Health Maintenance Organization)

HMO plans are strict about networks.

Rules include:

- You must choose a primary care physician

- You need referrals for specialists

- Out-of-network care is usually NOT covered

These plans usually have lower monthly premiums.

PPO (Preferred Provider Organization)

PPO plans offer more flexibility.

Benefits include:

- You can visit specialists without referrals

- Out-of-network care is allowed

- Larger provider networks

However, PPO plans usually have higher premiums.

EPO (Exclusive Provider Organization)

EPO plans are a mix between HMO and PPO.

Features include:

- No referrals required

- Must stay within network

- Out-of-network care usually not covered

POS (Point of Service)

POS plans combine HMO and PPO features.

They allow:

- Primary care physician management

- Some out-of-network coverage

- Referral system

Real-Life Example of In-Network vs Out-of-Network Costs

Let’s say you visit a specialist for a medical checkup.

In-Network Visit

Doctor charges: $300

Insurance negotiated rate: $180

Your copay: $40

You pay: $40

Out-of-Network Visit

Doctor charges: $300

Insurance coverage: 50%

You pay:

- $150 coinsurance

- Possible balance billing

Total you pay: $150 – $250

That’s a huge difference.

What Is Balance Billing?

Balance billing is one of the biggest reasons out-of-network doctors can be expensive.

Here’s how it works:

If a doctor charges $500 and insurance only allows $300, the doctor can bill you for the remaining $200.

This extra amount is called balance billing.

In-network doctors cannot do this because they agreed to negotiated prices.

When Out-of-Network Care Is Covered

Sometimes insurance will cover out-of-network services.

Common situations include:

- Medical emergencies

- No in-network specialist available

- Rural areas with limited providers

- Special medical treatments

Federal laws like the No Surprises Act also protect patients from certain surprise medical bills.

How to Check if a Doctor Is In-Network

Before scheduling an appointment, it’s smart to confirm whether a doctor is in your network.

Here’s how.

Check Your Insurance Website

Most insurers provide online provider directories.

You can search by:

- Doctor name

- Hospital

- Specialty

- ZIP code

Call the Doctor’s Office

Ask the receptionist:

“Do you accept my insurance plan?”

Make sure they accept your exact plan, not just the insurance company.

Contact Your Insurance Company

Call the number on your insurance card and ask if the provider is in network.

Tips to Avoid Out-of-Network Medical Bills

Healthcare costs in the United States can get expensive fast.

Here are some smart tips to avoid surprise charges.

Always Verify the Network

Even if the hospital is in-network, some specialists inside it may not be.

Examples include:

- Anesthesiologists

- Radiologists

- Pathologists

Use In-Network Hospitals

Hospitals often have both in-network and out-of-network doctors.

Ask ahead of time.

Get Referrals if Required

Some insurance plans require referrals for specialists.

Skipping this step may increase your costs.

Confirm Before Procedures

Before surgery or treatment, ask:

“Will every provider involved be in-network?”

Advantages of In-Network Doctors

Sticking with in-network providers has several benefits.

Lower Medical Costs

Insurance negotiated rates reduce healthcare expenses.

Less Paperwork

Doctors submit claims directly to your insurance company.

Predictable Pricing

Copays and coinsurance are usually clearly defined.

Easier Insurance Approval

Insurance companies approve treatments more easily within networks.

When Choosing an Out-of-Network Doctor Makes Sense

Sometimes patients still choose out-of-network providers.

Common reasons include:

- Specialized medical expertise

- Second medical opinions

- Preferred doctor not in network

- Faster appointment availability

In these cases, patients may pay more for the care they prefer.

FAQs About In-Network vs Out-of-Network Doctors

What happens if I accidentally see an out-of-network doctor?

You may receive a higher bill. Depending on your insurance plan, you might pay:

- Higher coinsurance

- Balance billing

- Full service cost

Always confirm network status before visiting a doctor.

Does emergency care count as out-of-network?

No. Emergency care is usually covered regardless of network status due to federal regulations.

However, follow-up care may need to be in network.

Why do out-of-network doctors charge more?

Because they do not have negotiated contracts with insurance companies, they can set their own prices.

Can I request in-network pricing from an out-of-network doctor?

Sometimes. Some doctors may agree to accept insurance negotiated rates, especially if you ask in advance.

How can I find cheap doctors within my insurance network?

Use your insurance provider’s online directory or healthcare marketplaces to find affordable in-network doctors near you.

Final Thoughts

Understanding in-network vs out-of-network doctors explained can save you hundreds—or even thousands—of dollars in medical bills.

The key takeaway is simple:

In-network doctors = lower costs.

Out-of-network doctors can be useful in certain situations, but they often come with higher expenses and more complicated insurance claims.

Before scheduling your next medical appointment, always:

- Check your insurance network

- Confirm provider participation

- Understand your plan’s coverage rules

Taking these small steps can protect your wallet and help you get the healthcare you need without unexpected bills.