Wondering why car insurance is so expensive? Learn what factors affect car insurance rates in America in this 2026 beginner-friendly guide with examples and tips.

You and your friend buy the same car… live in the same city… and even have similar jobs.

But when you both apply for car insurance, something doesn’t make sense:

- Your quote: $220/month

- Your friend’s quote: $140/month

Same situation… different price.

So what’s really going on behind the scenes?

Car insurance rates in the US aren’t random—they’re calculated based on multiple factors that most drivers don’t fully understand.

Let’s break everything down simply, clearly, and step-by-step so you know exactly what affects your premium—and how to lower it.

The Problem: Insurance Pricing Feels Confusing

Most drivers:

- Don’t know why prices vary

- Assume it’s unfair

- Overpay without realizing

The truth is:

Insurance companies use risk-based pricing—and every detail about you matters.

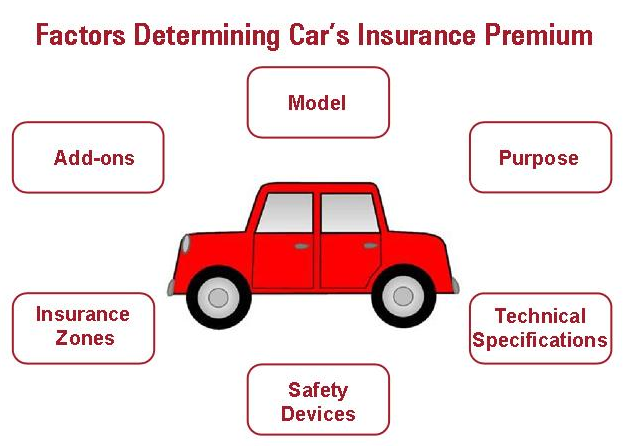

Top Factors That Affect Car Insurance Rates in America

Let’s explore the most important factors one by one.

1. Driving Record (BIGGEST FACTOR)

Your driving history is the #1 factor.

Affects your rate:

- Accidents

- Speeding tickets

- DUI offenses

Example

| Driving Record | Monthly Cost |

| Clean Record | $120 |

| One Accident | $180 |

| DUI | $300+ |

2. Age and Experience

Younger drivers = higher risk.

Why?

- Less experience

- Higher accident rates

Average Cost by Age

| Age | Monthly Cost |

| 16–20 | $250–$500 |

| 21–25 | $180–$300 |

| 30+ | $100–$180 |

3. Location (Where You Live)

Your ZIP code matters a lot.

Higher rates in:

- Big cities

- High crime areas

- Traffic-heavy regions

Example

| Location | Monthly Cost |

| Rural Area | $90 |

| Urban City | $200 |

4. Type of Car You Drive

Insurance companies consider:

- Car value

- Repair cost

- Theft rate

Expensive Cars = Higher Premiums

- Luxury cars

- Sports cars

- Electric vehicles

5. Credit Score (Important in the US)

In most states, insurers use credit-based scores.

Better credit = lower rates

Poor credit = higher rates

6. Coverage Level

More coverage = higher premium

Example

| Coverage Type | Monthly Cost |

| Liability Only | $80–$150 |

| Full Coverage | $180–$300 |

7. Mileage (How Much You Drive)

More driving = higher risk

Example

| Annual Miles | Cost Impact |

| 5,000 miles | Lower |

| 15,000 miles | Higher |

8. Claims History

Frequent claims = higher premiums

9. Marital Status

Married drivers often pay less.

10. Education & Occupation

Some insurers offer lower rates for:

- Professionals

- College graduates

Real-Life Example (Very Important)

John (age 22) vs Mike (age 35)

| Factor | John | Mike |

| Age | 22 | 35 |

| Driving Record | One accident | Clean |

| Credit Score | Average | Excellent |

Result:

- John pays: $280/month

- Mike pays: $130/month

Same car, different risk profile.

The Agitation: Why You Might Be Overpaying

You could be paying more because:

- Poor credit

- Old violations

- Wrong car choice

- Not comparing quotes

How to Lower Your Car Insurance Rates

Practical Tips

- Maintain clean driving record

- Improve credit score

- Choose affordable cars

- Increase deductible

- Compare multiple insurers

Risk vs Cost Table

| Risk Level | Monthly Cost |

| Low Risk | $100 |

| Medium Risk | $180 |

| High Risk | $300+ |

Beginner Tip (Must Read)

“Insurance companies don’t charge randomly—they price based on your risk level.”

Internal Resources (Learn More)

https://insurancesimplifiedusa.com

External Resources

- USA.gov Insurance Guide: https://www.usa.gov/insurance

- Insurance Information Institute: https://www.iii.org

- Consumer Finance Protection Bureau: https://www.consumerfinance.gov

Key Takeaways

- Driving record is the biggest factor

- Age, location, and car type heavily impact rates

- Credit score matters in most US states

- More coverage = higher cost

- Smart decisions can lower your premium

FAQs (SEO Optimized Section)

1. What is the biggest factor affecting car insurance rates?

Your driving record is the most important factor.

2. Does credit score affect insurance in the US?

Yes, in most states it significantly impacts rates.

3. Why is insurance higher for young drivers?

Due to higher accident risk and less experience.

4. Does the type of car affect insurance?

Yes, expensive or high-risk cars cost more to insure.

5. How can I lower my insurance cost?

Maintain good driving habits, improve credit, and compare quotes.

Conclusion

So, what factors affect car insurance rates in America?

It all comes down to risk.

Every detail—your driving record, age, car, location—tells insurers how likely you are to file a claim.

The good news?

- You can control many of these factors

- You can lower your rates over time

- You can make smarter insurance choices

Because the more you understand the system… the more you can beat it.

Sources

- USA.gov Insurance Resources

- Insurance Information Institute

- Consumer Financial Protection Bureau

- Industry data (2026 updates)

SEO Keywords (Ranking Boost)

what factors affect car insurance rates America 2026 guide, car insurance pricing explained simply US, insurance for beginners in the US, why is car insurance expensive USA, how to lower insurance rates US guide, cheap car insurance tips USA 2026