Copay vs Coinsurance: What’s the Difference? (Simple Guide for Americans)

If you’ve ever looked at a health insurance plan in the United States, you’ve probably seen terms like copay and coinsurance and wondered what they actually mean. Don’t worry—you’re definitely not the only one scratching your head over these insurance terms.

Understanding the difference between copay and coinsurance is super important because these costs determine how much money you pay when you visit a doctor, fill a prescription, or receive medical treatment.

In this simple guide, we’ll break down copay vs coinsurance, explain how each one works, and give real-life examples so you can understand your health insurance costs without the confusion.

What Is a Copay?

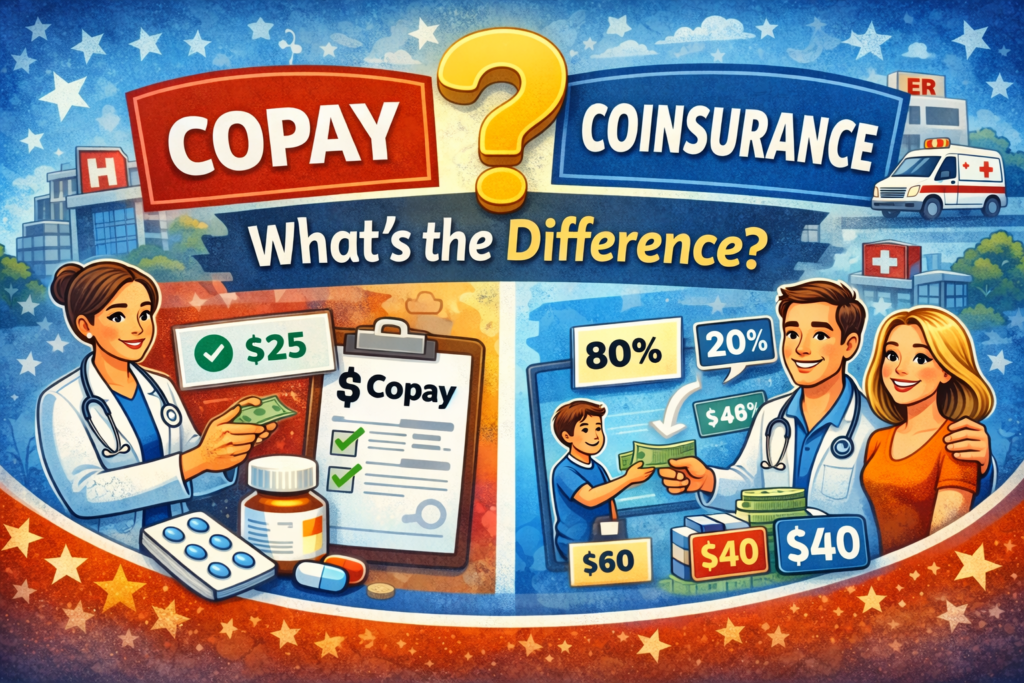

A copay (copayment) is a fixed amount of money you pay for a medical service or prescription medication.

No matter how expensive the service is, your copay stays the same.

For example:

- $25 for a doctor visit

- $10 for generic prescription drugs

- $50 for a specialist visit

- $100 for an emergency room visit

Your insurance company pays the remaining cost after your copay.

Most modern insurance plans created under the Affordable Care Act include copays for routine medical services.

Example of a Copay

Let’s say your health insurance plan has:

- Primary doctor copay: $30

You go to the doctor for a checkup and the total bill is $150.

Here’s how it works:

- You pay: $30 copay

- Insurance pays: $120

Your payment stays the same regardless of the total cost of the visit.

Pretty simple, right?

What Is Coinsurance?

Coinsurance works differently.

Instead of paying a fixed fee, coinsurance is a percentage of the medical bill you must pay after meeting your deductible.

For example:

- 10% coinsurance

- 20% coinsurance

- 30% coinsurance

Your insurance company pays the rest of the bill.

Most U.S. insurance plans apply coinsurance after the deductible is reached.

Example of Coinsurance

Let’s say your health insurance plan includes:

- Deductible: $1,000

- Coinsurance: 20%

After you’ve already paid your $1,000 deductible, you receive a hospital bill for $2,000.

Here’s how coinsurance works:

- You pay 20% of $2,000 = $400

- Insurance pays 80% = $1,600

This cost-sharing structure is common in plans offered through the Health Insurance Marketplace.

Copay vs Coinsurance: Key Differences

Let’s make it crystal clear.

| Feature | Copay | Coinsurance |

|---|---|---|

| Payment type | Fixed amount | Percentage of bill |

| Cost example | $25 doctor visit | 20% of hospital bill |

| Predictability | Easy to predict | Varies depending on bill |

| When it applies | Often before deductible | Usually after deductible |

| Common services | Doctor visits, prescriptions | Surgeries, hospital stays |

In short:

Copay = flat fee

Coinsurance = percentage of cost

When Do You Pay Copay vs Coinsurance?

Both costs can apply in the same insurance plan.

Here’s a typical situation.

Before Meeting Deductible

You might pay:

- Full cost of services

- Some copays depending on the plan

After Meeting Deductible

You may pay:

- Copays for routine services

- Coinsurance for expensive procedures

Real-Life Example: Copay vs Coinsurance Together

Let’s walk through a simple real-life example.

Sarah has a health insurance plan with:

- Deductible: $1,500

- Doctor visit copay: $25

- Coinsurance: 20%

Step 1: Doctor Visit

Sarah visits her doctor.

Total bill: $200

She pays:

- $25 copay

Insurance covers the rest.

Step 2: Medical Procedure

Later, Sarah needs a medical procedure costing $3,000.

Since she hasn’t met her deductible yet:

- She pays $1,500 deductible

Remaining bill:

$3,000 – $1,500 = $1,500

Coinsurance applies:

- Sarah pays 20% = $300

- Insurance pays $1,200

This example shows how copays and coinsurance can work together in one plan.

What Is an Out-of-Pocket Maximum?

Another important term related to copays and coinsurance is the out-of-pocket maximum.

This is the maximum amount you must pay for covered medical services in a year.

Once you reach that limit:

- Your insurance pays 100% of covered services

This rule was established by regulations under the Affordable Care Act.

Example:

Out-of-pocket maximum: $8,000

After you spend $8,000 in deductibles, copays, and coinsurance:

Insurance covers all additional healthcare costs for the rest of the year.

Pros and Cons of Copays

Advantages

- Easy to understand

- Predictable costs

- Budget-friendly for routine care

Disadvantages

- Still adds up over time

- Some plans have high copays for specialists

Pros and Cons of Coinsurance

Advantages

- Lower monthly premiums in some plans

- Cost sharing between patient and insurer

Disadvantages

- Bills can become expensive quickly

- Harder to predict healthcare costs

Typical Copay and Coinsurance Costs in the U.S.

Here are average amounts found in many American insurance plans.

Common Copays

- $20–$40 primary doctor visit

- $40–$75 specialist visit

- $10–$25 generic prescriptions

- $75–$150 emergency room visit

Common Coinsurance Rates

- 10% coinsurance

- 20% coinsurance

- 30% coinsurance

Higher coinsurance percentages usually mean lower monthly premiums.

Tips to Save Money on Copays and Coinsurance

Healthcare costs can add up fast, but these tips can help.

Stay In-Network

Doctors in your insurance network cost significantly less.

Use Preventive Care

Many preventive services are free under the Affordable Care Act.

Choose Generic Medications

Generic drugs can save hundreds of dollars annually.

Review Your Plan Each Year

Insurance plans change yearly, so compare options during open enrollment.

Frequently Asked Questions (FAQs)

Is copay better than coinsurance?

It depends. Copays are easier to predict, while coinsurance can vary based on the total medical bill.

Do I pay both copay and coinsurance?

Sometimes yes. Many insurance plans include both copays for routine care and coinsurance for larger medical expenses.

Does coinsurance apply before the deductible?

Usually no. Most insurance plans require you to meet your deductible before coinsurance applies.

Are prescription drugs covered by copays?

Yes. Many insurance plans charge fixed copays for prescription medications.

Can I avoid copays and coinsurance completely?

Not entirely. However, once you reach your out-of-pocket maximum, your insurance typically covers 100% of eligible medical expenses.

Final Thoughts

Understanding the difference between copay and coinsurance is key to managing healthcare costs in the United States.

Here’s the simple takeaway:

- Copay: Fixed fee you pay for medical services

- Coinsurance: Percentage of the medical bill you share with insurance

Both costs are part of the modern healthcare system and are designed to split expenses between patients and insurance providers.

By learning how these costs work, you can make smarter decisions when choosing a health insurance plan and avoid unexpected medical bills.

And remember—taking advantage of preventive services required under the Affordable Care Act can help you stay healthy while saving money.