Health Insurance Deductible Explained (With Real-Life Example) – Simple Guide for Americans

If you’ve ever looked at a health insurance plan in the United States, you’ve probably seen the word deductible and thought, “Wait… what does that actually mean?”

Don’t worry—you’re not alone. Many Americans get confused by insurance terms like deductibles, copays, and coinsurance. But understanding your deductible is super important because it directly affects how much money you pay for healthcare.

In this guide, we’ll break down what a health insurance deductible is, how it works, and a real-life example so you can finally understand it without the headache.

What Is a Health Insurance Deductible?

A health insurance deductible is the amount of money you must pay out of your own pocket for medical services before your insurance company starts paying.

Think of it like this:

Your deductible is the entry ticket to your insurance benefits.

Until you pay that amount, you’re responsible for most healthcare costs.

For example:

- If your deductible is $1,500, you must pay the first $1,500 of medical expenses before insurance begins sharing the cost.

After that, your insurance kicks in and starts covering a large portion of your healthcare bills.

Many U.S. health plans regulated by the Affordable Care Act follow this structure.

Why Deductibles Exist in Health Insurance

Insurance companies use deductibles for a few important reasons:

1. To Reduce Unnecessary Medical Visits

If insurance paid 100% from day one, people might visit the doctor for every tiny issue.

Deductibles encourage patients to be more mindful about healthcare spending.

2. To Keep Monthly Premiums Lower

Plans with higher deductibles usually have lower monthly premiums.

This means you pay less each month but more when you actually need care.

3. To Share Healthcare Costs

Deductibles ensure that both the insurance company and the policyholder share responsibility for medical costs.

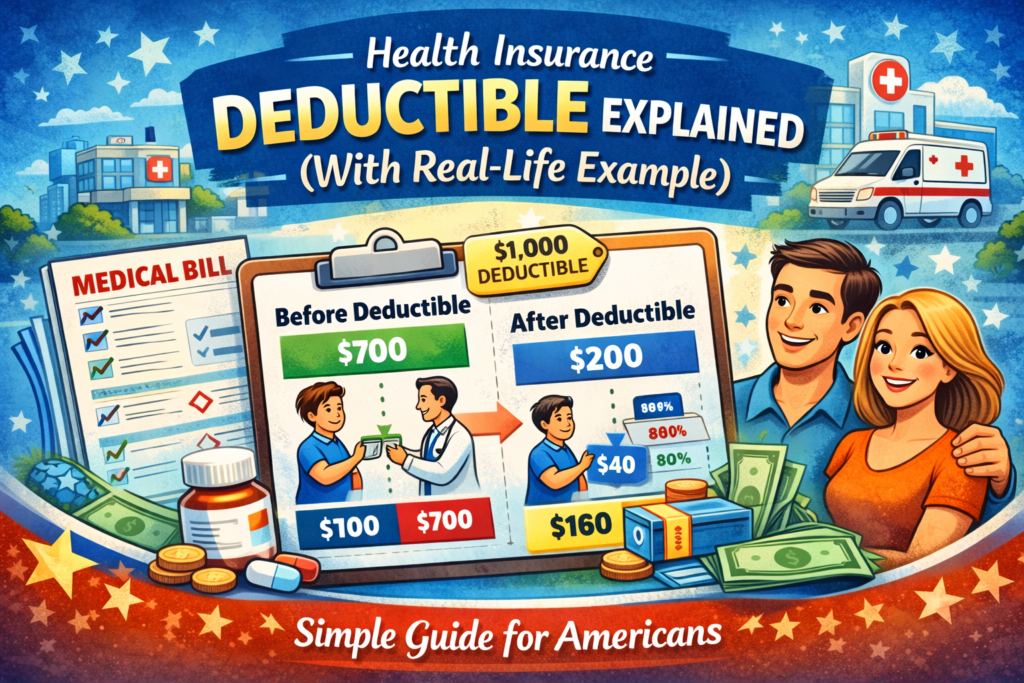

Simple Real-Life Example of a Deductible

Let’s walk through a real-world example to make things crystal clear.

Example Scenario

John has a health insurance plan with:

- Deductible: $1,000

- Coinsurance: 20%

- Out-of-pocket maximum: $6,000

Now let’s say John needs medical treatment.

Step 1: First Medical Bill

John visits the hospital and the bill comes to $700.

Since he hasn’t met his deductible yet:

- John pays $700

- Remaining deductible: $300

Insurance pays $0 at this stage.

Step 2: Second Medical Bill

Later, John needs another treatment costing $500.

Here’s how it works:

- John pays the remaining $300 deductible

- Insurance starts covering the rest

Remaining bill after deductible:

$500 – $300 = $200

Now coinsurance applies.

Insurance pays 80% ($160)

John pays 20% ($40)

Step 3: After Deductible Is Met

Now that John has paid the full $1,000 deductible, insurance will share the costs for future medical bills.

From this point forward:

- Insurance pays most of the bill

- John only pays coinsurance or copays

Pretty straightforward, right?

Average Health Insurance Deductibles in the U.S.

Deductibles vary depending on the type of insurance plan.

Here’s a rough idea of typical deductibles in the United States.

Individual Plans

- Low deductible: $500 – $1,500

- Average deductible: $1,500 – $3,000

- High deductible: $4,000 – $8,000

Family Plans

Family deductibles are usually higher:

- Average: $3,000 – $8,000

Some plans even reach $10,000+ for family coverage.

High deductible plans are often paired with Health Savings Account, which lets people save money tax-free for medical expenses.

Types of Health Insurance Deductibles

Not all deductibles work the same way.

Here are the most common types.

Individual Deductible

This applies to one person in an insurance plan.

Once that person reaches the deductible, their insurance coverage begins.

Family Deductible

Family plans have a combined deductible for all members.

Example:

Family deductible = $6,000

Once the family spends $6,000 collectively, insurance starts paying for everyone.

Embedded Deductible

In this system:

- Each family member has an individual deductible

- There is also a family deductible

Once one person reaches their personal deductible, insurance begins covering them—even if the family deductible hasn’t been reached.

Non-Embedded Deductible

Here, the entire family deductible must be met before insurance pays anything.

This type is less common but still exists in some plans.

High Deductible Health Plans (HDHP)

A High Deductible Health Plan (HDHP) has a larger deductible but lower monthly premiums.

For 2026, HDHPs usually have deductibles of:

- Around $1,600+ for individuals

- Around $3,200+ for families

These plans are often combined with **Health Savings Account benefits.

Advantages include:

- Lower monthly premiums

- Tax savings

- Long-term healthcare savings

But they also mean higher upfront costs when you need care.

What Services Are Covered Before the Deductible?

Good news: not everything requires meeting your deductible first.

Under the Affordable Care Act, many preventive services are free.

These include:

- Annual checkups

- Vaccinations

- Blood pressure screenings

- Cholesterol tests

- Cancer screenings

- Mammograms

- Colonoscopies

These services are typically covered 100%, even if you haven’t met your deductible.

Deductible vs Copay vs Coinsurance

These three terms often confuse people.

Let’s simplify them.

Deductible

Amount you pay before insurance starts paying.

Copay

A fixed fee you pay for certain services.

Example:

- $25 doctor visit

- $15 prescription medication

Coinsurance

A percentage of the bill you pay after meeting the deductible.

Example:

Insurance pays 80%, you pay 20%.

Understanding these three costs helps you estimate your total healthcare spending.

Tips to Manage Your Deductible Smartly

Healthcare can get expensive, but these tips can help you stay ahead.

1. Use Preventive Care

Take advantage of free screenings and checkups.

2. Stay In-Network

Doctors within your insurance network usually cost less.

3. Use Generic Medications

Generic drugs are much cheaper than brand-name versions.

4. Open a Health Savings Account

If you qualify, a **Health Savings Account can help you save tax-free for healthcare expenses.

5. Track Your Medical Spending

Keep track of bills so you know when you’re close to reaching your deductible.

Frequently Asked Questions (FAQs)

What happens after I meet my deductible?

Once you meet your deductible, your insurance company starts paying a large portion of your medical bills. You may still pay copays or coinsurance.

Do I pay my deductible every time I visit a doctor?

No. You only pay medical costs until the deductible amount is reached. After that, insurance begins sharing the costs.

Does the deductible reset every year?

Yes. Most health insurance deductibles reset once per year, usually on January 1.

Are prescriptions included in the deductible?

Some plans include prescription drugs in the deductible, while others offer copays for medications before the deductible is met.

Is a higher deductible better?

It depends on your situation.

High deductibles usually mean:

- Lower monthly premiums

- Higher medical costs when you need care

Low deductibles mean:

- Higher monthly premiums

- Lower out-of-pocket medical costs

Final Thoughts

Understanding your health insurance deductible is one of the most important parts of managing healthcare costs in the United States.

Your deductible determines how much you must pay before insurance begins covering medical expenses, so knowing how it works can help you avoid surprise bills.

Whether you choose a low-deductible plan for predictable costs or a high-deductible plan with lower premiums, the key is to pick a plan that matches your healthcare needs and budget.

And remember: taking advantage of preventive care services covered under the Affordable Care Act can help keep you healthy while saving money