Term Life vs Whole Life Insurance Explained (Complete Guide for Americans – 2026)

If you’ve ever tried to shop for life insurance in the United States, you’ve probably run into two major options: term life insurance and whole life insurance.

At first glance, they might sound pretty similar. After all, both offer financial protection for your loved ones. But once you dig a little deeper, you’ll realize these two policies work very differently.

Many Americans searching online for “term life vs whole life insurance explained” or “which life insurance policy is best in the USA” are simply trying to understand which option makes the most sense for their family and financial goals.

In this guide, we’ll break down everything you need to know about term life insurance vs whole life insurance, including how they work, their pros and cons, costs, and which policy might be right for you.

So grab a coffee and let’s make life insurance simple.

What Is Life Insurance?

Before comparing term and whole life insurance, let’s quickly cover the basics.

Life insurance is a financial contract between you and an insurance company. You pay regular premiums, and in return, the insurer agrees to pay a death benefit to your beneficiaries if you pass away.

Your beneficiaries might include:

- Your spouse

- Children

- Parents

- Business partners

- Anyone you choose

The payout can help cover major expenses like:

- Mortgage payments

- Living expenses

- Debt repayment

- College tuition

- Funeral costs

This financial safety net is why millions of Americans invest in life insurance.

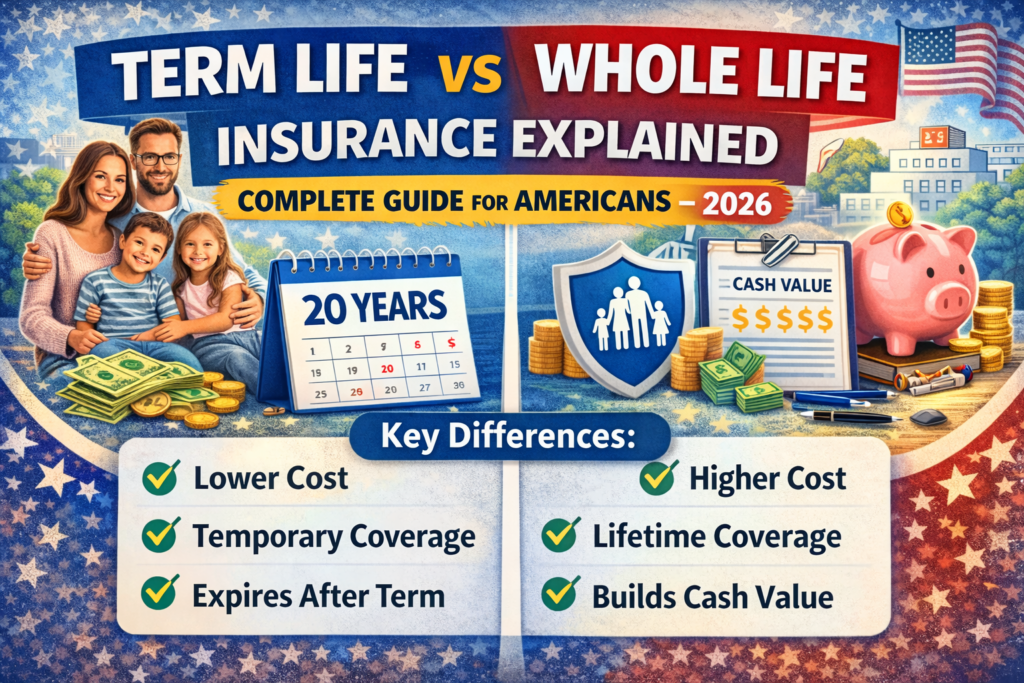

What Is Term Life Insurance?

Term life insurance is the simplest and most affordable type of life insurance in the United States.

As the name suggests, it provides coverage for a specific term or time period.

Common term lengths include:

- 10 years

- 20 years

- 30 years

If the policyholder passes away during that term, the beneficiaries receive the death benefit.

If the policy expires while the policyholder is still alive, the coverage ends unless it’s renewed.

Example

Let’s say you purchase:

- $500,000 term life insurance policy

- 20-year term

If you pass away within those 20 years, your beneficiaries receive $500,000.

If you outlive the term, the policy simply expires.

Key Features of Term Life Insurance

Term life insurance is popular because of its simplicity.

Main characteristics:

- Fixed coverage period

- Lower premiums

- No investment component

- Straightforward protection

Many financial experts recommend term life insurance for young families and new homeowners.

Benefits of Term Life Insurance

Here are some of the biggest advantages.

Affordable Premiums

Term life insurance is usually the cheapest life insurance option in the USA.

Because it only provides coverage for a limited time, insurers can keep premiums low.

Simple and Easy to Understand

There are no complicated investment features.

You simply pay premiums and receive coverage.

High Coverage for Lower Cost

You can often get $500,000 or even $1 million in coverage at a relatively low monthly premium.

Ideal for Temporary Financial Needs

Term life works well for financial obligations such as:

- Raising children

- Paying off a mortgage

- Covering student loans

Downsides of Term Life Insurance

While term life is affordable, it does have some limitations.

No Cash Value

Term life policies do not build savings or investment value.

Coverage Eventually Expires

Once the term ends, you may need to buy a new policy at a higher price.

Premiums Increase With Age

If you renew or buy a new policy later in life, the cost may rise significantly.

What Is Whole Life Insurance?

Whole life insurance provides lifetime coverage rather than temporary protection.

As long as you continue paying premiums, the policy remains active for your entire life.

But whole life insurance offers something extra: cash value accumulation.

This means part of your premium goes into a savings-like account that grows over time.

Key Features of Whole Life Insurance

Whole life policies include several unique characteristics.

Lifetime Coverage

Unlike term life, whole life policies never expire as long as premiums are paid.

Cash Value Growth

A portion of your premium builds tax-deferred savings.

This money can be borrowed against or withdrawn.

Fixed Premiums

Premium payments remain the same throughout the life of the policy.

Guaranteed Death Benefit

Your beneficiaries will receive a payout whenever you pass away.

Benefits of Whole Life Insurance

Whole life insurance offers several long-term financial advantages.

Permanent Protection

You never have to worry about your coverage expiring.

Cash Value Savings

Your policy builds value over time that you can use during your lifetime.

Financial Planning Tool

Some people use whole life policies for:

- Retirement planning

- Estate planning

- Wealth transfer

Stable Premiums

Unlike term policies that may increase later, whole life premiums remain fixed.

Downsides of Whole Life Insurance

Whole life insurance isn’t perfect.

Here are some potential drawbacks.

Higher Premiums

Whole life insurance can cost 5 to 10 times more than term life insurance.

Slower Cash Value Growth

The savings portion may grow slower than other investment options.

More Complex Policy Structure

Whole life policies can be harder to understand compared to simple term life coverage.

Term Life vs Whole Life Insurance (Side-by-Side Comparison)

Here’s a quick breakdown of the key differences.

Term Life Insurance

Best for:

- Affordable coverage

- Temporary financial protection

- Young families

- Budget-conscious buyers

Key points:

- Lower premiums

- Fixed coverage term

- No cash value

- Simple structure

Whole Life Insurance

Best for:

- Lifetime coverage

- Wealth planning

- Long-term financial strategies

Key points:

- Higher premiums

- Permanent protection

- Cash value accumulation

- Fixed premium payments

Which Life Insurance Is Better in the USA?

There’s no universal answer to this question. It depends on your financial goals.

Term Life Is Best For

- Young parents

- New homeowners

- Families with limited budgets

- Income replacement protection

Whole Life Is Best For

- Long-term wealth planning

- High-income individuals

- Estate planning strategies

- People wanting lifetime coverage

Many financial advisors actually recommend a “buy term and invest the difference” strategy.

This means buying affordable term insurance and investing the money saved elsewhere.

How Much Life Insurance Do Americans Typically Need?

Experts often recommend coverage equal to 10–15 times your annual income.

For example:

If you earn $70,000 per year, a recommended policy might be:

$700,000 – $1,000,000 in coverage.

Consider these factors when calculating coverage:

- Mortgage balance

- Living expenses

- Children’s education

- Debt obligations

- Future financial goals

How Much Does Life Insurance Cost?

Life insurance costs vary based on several factors.

These include:

- Age

- Health

- Lifestyle

- Smoking status

- Coverage amount

Typical Monthly Premiums

Term life insurance:

- $20 – $50 per month (young healthy adults)

Whole life insurance:

- $200 – $600 per month depending on coverage.

Tips for Choosing the Best Life Insurance Policy

If you’re shopping for life insurance in the USA, keep these tips in mind.

Compare Multiple Insurance Companies

Rates can vary widely between insurers.

Buy Insurance While You’re Young

Premiums increase as you age.

Be Honest on Your Application

Providing accurate health information prevents claim issues later.

Choose the Right Coverage Amount

Make sure your policy covers your family’s financial needs.

Frequently Asked Questions

Is term life insurance better than whole life insurance?

Term life insurance is often better for affordability and simple income protection, while whole life insurance is better for long-term financial planning.

Can I convert term life insurance to whole life?

Some insurance companies offer term-to-whole life conversion options without requiring a medical exam.

What happens if I outlive my term life policy?

The coverage ends, but some policies allow renewal or conversion to permanent insurance.

Is whole life insurance a good investment?

Whole life insurance can build cash value, but it typically grows slower than traditional investments like stocks or retirement accounts.

Can you have both term and whole life insurance?

Yes. Many Americans combine both policies to balance affordability and permanent coverage.

Final Thoughts

Understanding the difference between term life vs whole life insurance is an important step toward protecting your family’s financial future.

If you’re looking for affordable coverage and income protection, term life insurance is often the best option.

If you want lifetime coverage with a savings component, whole life insurance may fit your long-term financial goals.

The most important step is simply getting coverage in place. Life is unpredictable, and having the right policy can give you peace of mind knowing your loved ones will be financially protected.

In the end, life insurance isn’t just about money — it’s about taking care of the people who matter most.