What Is Minimum Car Insurance in the USA? (Complete 2026 Guide)

If you drive a car in the United States, car insurance isn’t just a good idea — it’s the law in most states. But here’s the catch: not every driver needs the same level of coverage. Many Americans start with something called minimum car insurance.

So what exactly does that mean?

Simply put, minimum car insurance is the lowest amount of coverage required by law in your state to legally drive a vehicle. It’s designed to cover basic damages if you cause an accident — mainly the injuries and property damage you might cause to others.

In this guide, we’ll break down what minimum car insurance in the USA actually covers, how it works, how much it costs, and whether it’s really enough for you.

Let’s dive in.

What Is Minimum Car Insurance?

Minimum car insurance refers to the legal minimum amount of liability coverage required by each U.S. state.

This coverage is designed to protect other drivers and their property if you cause an accident.

Important thing to know:

Minimum insurance usually does NOT cover your own car or injuries.

That’s why many drivers call it “liability-only insurance.”

Minimum Coverage Typically Includes

Most states require at least two types of coverage:

- Bodily Injury Liability

- Property Damage Liability

These two cover damages you cause to other people, not yourself.

Understanding Liability Coverage

Let’s break it down so it’s crystal clear.

1. Bodily Injury Liability

This covers medical expenses, lost wages, and legal costs if someone gets injured in an accident you caused.

It may pay for:

- Hospital bills

- Doctor visits

- Physical therapy

- Lost income

- Legal defense if you’re sued

2. Property Damage Liability

This pays for damage to someone else’s property.

Examples include:

- Another person’s car

- Fences

- Buildings

- Street signs

- Utility poles

So if you accidentally crash into someone’s car or a mailbox, property damage liability covers the repairs.

How Minimum Car Insurance Is Written

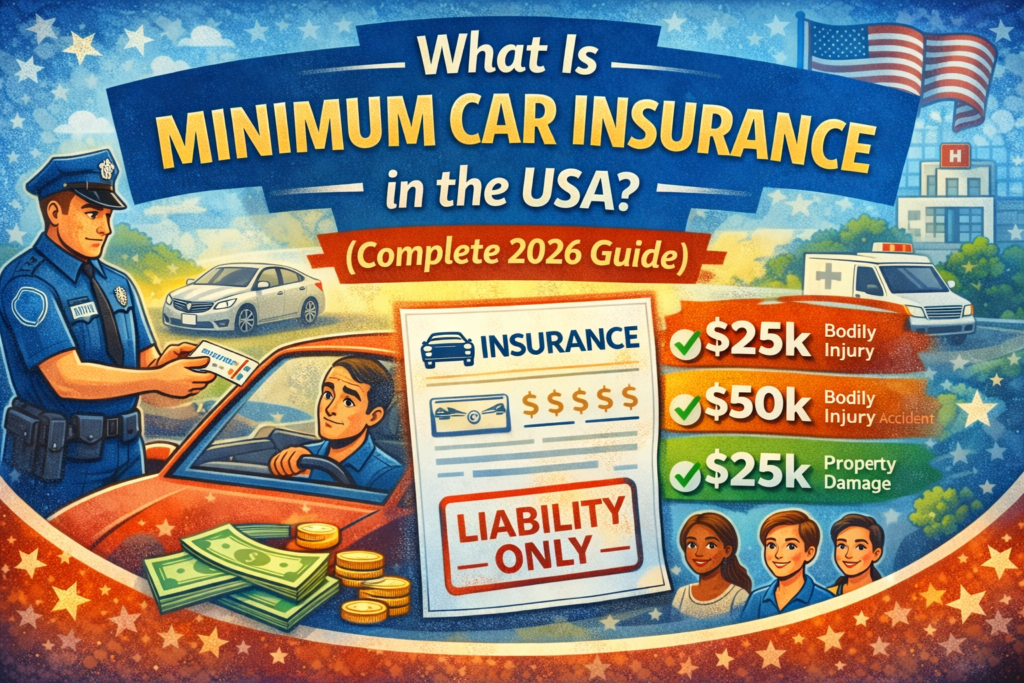

In the U.S., insurance coverage is usually written in three numbers like this:

25/50/25

Here’s what that means:

- $25,000 bodily injury coverage per person

- $50,000 bodily injury coverage per accident

- $25,000 property damage coverage

So if you cause an accident that injures two people, your insurance would cover up to $50,000 total for their medical expenses.

Anything beyond that amount?

You may have to pay out of pocket.

Minimum Insurance Requirements by State

Each state sets its own insurance laws, so minimum requirements vary.

Here are a few examples:

California

Minimum coverage:

- $15,000 bodily injury per person

- $30,000 bodily injury per accident

- $5,000 property damage

Texas

Minimum coverage:

- $30,000 bodily injury per person

- $60,000 bodily injury per accident

- $25,000 property damage

Florida

Florida requires:

- $10,000 personal injury protection (PIP)

- $10,000 property damage liability

New York

Minimum requirements:

- $25,000 bodily injury per person

- $50,000 bodily injury per accident

- $10,000 property damage

Because laws differ, it’s always smart to check your state’s insurance requirements.

What Minimum Car Insurance Does NOT Cover

Here’s the big surprise for many drivers.

Minimum car insurance does not cover your own vehicle in most cases.

It also doesn’t include several other important protections.

Not Included in Minimum Coverage

- Repairs to your car

- Theft

- Vandalism

- Natural disasters

- Medical bills for you

- Hit-and-run accidents

- Uninsured drivers

To get these protections, drivers usually add extra coverage like:

- Collision insurance

- Comprehensive insurance

- Uninsured motorist coverage

How Much Does Minimum Car Insurance Cost?

Minimum coverage is the cheapest type of car insurance in the United States.

Average monthly costs typically range from:

- $40 to $100 per month

However, your actual premium depends on several factors.

Factors That Affect Insurance Cost

Insurance companies look at things like:

- Your age

- Driving record

- Location

- Credit score

- Type of car

- Annual mileage

- Insurance history

For example:

- A safe driver in their 30s may pay $50/month

- A teenage driver might pay $200/month or more

Insurance pricing can vary a lot.

Pros of Minimum Car Insurance

Many drivers choose minimum coverage because it’s affordable.

Benefits

Lower Monthly Premiums

Minimum policies are the cheapest option available.

Legal Compliance

It allows you to legally drive in your state.

Good for Older Vehicles

If your car is old and not worth much, minimum coverage might make financial sense.

Simple Policy

Fewer coverage types mean simpler insurance.

Cons of Minimum Car Insurance

While minimum insurance is affordable, it comes with risks.

Downsides

Limited Protection

If damages exceed coverage limits, you must pay the rest yourself.

No Coverage for Your Car

Your vehicle repairs won’t be covered.

Higher Financial Risk

Serious accidents can cost tens or hundreds of thousands of dollars.

Possible Lawsuits

If insurance limits are exceeded, victims may sue you.

Because of these risks, many financial experts recommend higher liability limits.

Real-Life Example of Minimum Insurance

Let’s say Alex has a minimum policy of 25/50/25.

He accidentally causes a crash that results in:

- $40,000 medical bills for one driver

- $30,000 medical bills for another

- $20,000 car damage

Here’s what happens:

Insurance pays:

- $25,000 for the first driver

- $25,000 for the second driver (because the per accident limit is $50,000)

- $20,000 property damage covered

But Alex must pay:

- $15,000 out of pocket for the remaining medical costs.

That’s why minimum coverage can be risky.

Additional Coverage Many Americans Buy

To stay better protected, many drivers add extra coverage.

Popular Optional Coverages

Collision Insurance

Covers damage to your car after accidents.

Comprehensive Insurance

Protects against:

- Theft

- Fire

- Floods

- Vandalism

- Animal collisions

Uninsured Motorist Coverage

Protects you if the other driver has no insurance.

Medical Payments Coverage

Helps pay medical bills for you and passengers.

These add-ons provide stronger financial protection.

Who Should Consider Minimum Car Insurance?

Minimum coverage may work well for certain drivers.

Good Candidates

- Drivers with older cars

- People on tight budgets

- Those who rarely drive

- Vehicles with low resale value

However, people with valuable assets should consider higher coverage limits.

Tips for Getting Cheap Minimum Car Insurance

Want to keep your insurance bill low? Try these strategies.

Smart Ways to Save

- Compare quotes from multiple insurers

- Maintain a clean driving record

- Bundle home and auto insurance

- Increase your deductible

- Ask about safe driver discounts

- Drive fewer miles annually

Shopping around can sometimes save hundreds of dollars per year.

FAQs About Minimum Car Insurance

Is minimum car insurance enough?

It’s legally enough, but financially it may not fully protect you in serious accidents.

Is minimum insurance the cheapest option?

Yes. Minimum coverage is usually the lowest-cost policy available.

Do all states require car insurance?

Most states do, but a few allow alternatives like financial responsibility bonds.

Can I drive without insurance in the USA?

In most states, driving without insurance is illegal and can result in:

- Fines

- License suspension

- Vehicle impoundment

Can I upgrade my insurance later?

Yes. You can increase coverage anytime or during your policy renewal.

Final Thoughts

Minimum car insurance in the United States provides basic legal protection, but it comes with limited coverage.

Here’s the quick breakdown:

Minimum insurance typically covers:

- Injuries you cause to others

- Damage to someone else’s property

It usually does NOT cover your car or medical bills.

While minimum coverage keeps costs low, it can leave drivers financially exposed after serious accidents.

That’s why many Americans choose higher liability limits or full coverage insurance for better protection.

At the end of the day, the best policy is one that balances affordability with enough coverage to protect your finances.